TABLE OF CONTENTS

- What is a startup business loan?

- What are the different types of loans for startups?

- What are the best reasons for getting startup business loans?

- What do lenders factor in when assessing you for startup loans?

- Should you go with a traditional bank or another type of lender?

- What do you need to provide when applying for a start up business loan?

- Can you get an unsecured loan for your business idea?

- 4 steps to accessing a business loan

If you’ve ever taken the leap and started a new business, you already know that securing funding can be one of the biggest challenges in those early days. But a start up business loan can give you the financial support and structure to launch or expand your exciting venture. There are lots of different loans out there, with each one catering to different needs and business stages.

So let’s get stuck in and cover everything you need to know about how budding small business owners can secure business lending.

What is a startup business loan?

A startup business loan is essentially funding that’s needed for you to start or grow a new venture. This type of business loan is generally considered higher risk for lenders since new businesses tend to lack a financial track record and may not even have any customers yet.

Because of this, you’ll find that most startup loans have far stricter eligibility criteria, and you can probably expect to be slapped with a higher interest rate than what you might get with personal loans. However, a startup loan can be instrumental in helping you buy essential inventory, get a lease for your workspace, or simply take care of day-to-day operational costs.

Unlike traditional business loans given to established companies, your startup loan will likely rely on your credit history and assets. In other words, your personal financial stability can be the make-or-break of getting a loan approved.

What are the different types of loans for startups?

Got a clever business idea? Lenders will want to hear about it. That’s why there are several different types of small business loans available for startups, each with its own pros and cons. Some of the most popular types include:

- Term loans: A lump sum that you borrow with fixed repayments over a set period. Whether they are secured or unsecured, they are for taking care of one-time, larger expenses.

- Business line of credit: Similar to a credit card, a line of credit gives you ongoing access to funds up to a certain limit. You only pay interest on the amount you use, which is handy for startups with fluctuating expenses.

- Equipment financing: Used to finance the purchase of equipment or machinery, with the asset itself serving as collateral.

- Invoice financing: Lets startups borrow against unpaid invoices, which is helpful for managing your cash flow or dealing with seasonality.

- Merchant cash advance: A cash advance based on future sales, with repayments linked to a percentage of your daily sales. While less common, businesses that have regular, card-based revenue could find this the most appropriate loan type.

What are the best reasons for getting startup business loans?

You probably have very good reasons for being interested in a business startup loan. But for the sake of clarity, here are some of the more common motivations:

![]()

Buying inventory

Keeping inventory stocked is the ‘bread and butter’ for businesses that sell physical products. Loans can help you secure bulk orders, get discounts from suppliers and manage seasonal fluctuations.

![]()

Covering marketing costs

A strong marketing push can attract new customers and generate much-needed revenue in the early days of your business. Startup business loans can fund digital advertising, influencer collaborations, branding initiatives, and more.

![]()

Product development

Creating a new product can be very expensive – from ideation to prototyping to bringing something to market. Having a loan means your own business can fund the design, development and testing phases – and beyond.

![]()

Purchasing equipment

Business loans can be used to finance essential equipment purchases, from industrial machinery to office suppliers and everything in between.

![]()

Hiring talent

Growing businesses need skilled employees. A startup business loan can help you cover the cost of recruiting and training.

What do lenders factor in when assessing you for startup loans?

When reviewing your application, lenders will look at a number of different areas to gauge whether your startup is not only viable, but will have the ability to repay the loan.

Credit score: Personal credit scores play a much bigger role than you might expect, especially for new businesses. Lenders want to see you display responsible credit management.

Business plan: A fully detailed business plan detailing the startup model, revenue projections and market strategy are a must. You want to make sure the lender understands your startup’s goals and long-term potential.

Industry experience: Having prior experience or a successful track record in a related industry can positively influence a lender’s decision.

Personal investment: Lenders look for evidence (i.e. financial statements) that you have invested your own funds and personal assets, which shows commitment to the venture’s success.

Collateral: Collateral (e.g. real estate or equipment) reduces the risk on the lender and can ultimately improve your chances of being approved or getting better terms.

Should you go with a traditional bank or another type of lender?

For startups, choosing the right lender can make a big difference. Traditional banks, for example, could offer lower interest rates but have stricter lending criteria and a lengthy application process. Expect them to demand excellent credit and strong financials.

Otherwise there are places like credit unions, which might have more competitive rates and flexible loan terms. However, they also tend to have a more stringent approval process in case your business fails.

These days, you can also get funding from online lenders, who generally have faster application processes and are more lenient with their eligibility requirements. But expect interest rates to be higher for startups.

You might also be interested in peer-to-peer (P2P) lenders. P2P lending platforms connect borrowers with individual investors, and they could be a viable option for startups. Ultimately, every lender type has benefits and drawbacks, so do your due diligence before locking yourself into a loan contract.

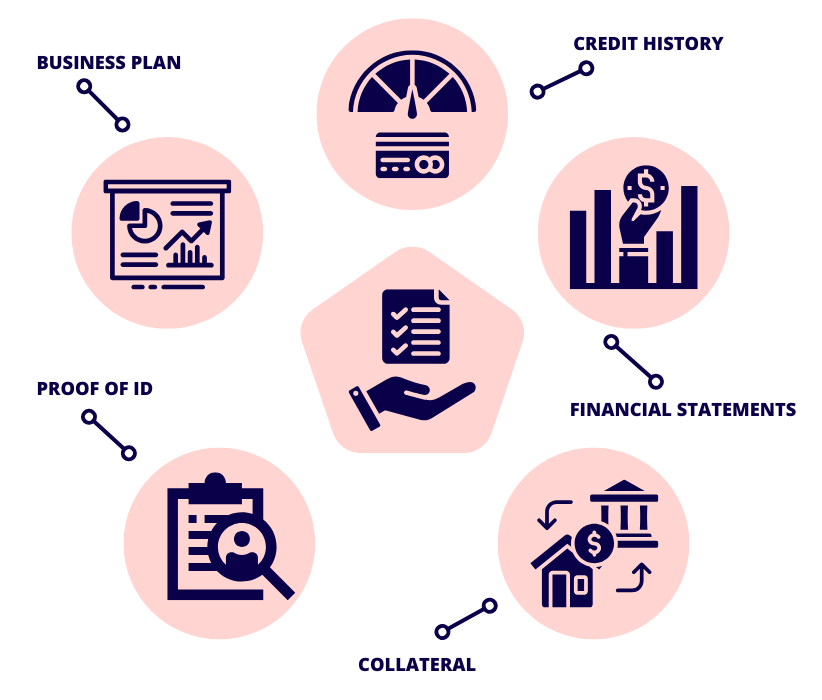

What do you need to provide when applying for a start up business loan?

- Detailed business plan: A structured business plan walks lenders through your business model, financial projections, market analysis, and growth strategy.

- Credit history: Both personal and business credit history (if available).

- Financial statements: Personal and business tax returns, income statements, as well as cash flow forecasts will give lenders a snapshot into your financial health.

- Proof of collateral: If you’re applying for a secured loan, you’ll need documents detailing the value of any proposed collateral.

- Identification: Proof of identity and ownership, including your Australian Business Number (ABN) and business registration details.

Can you get an unsecured loan for your business idea?

Yes, it is possible to get an unsecured business loan as a startup, but it will be much more challenging. Unsecured loans don’t require collateral, which makes them riskier for lenders. To compensate, lenders might offer these loans with higher interest rates or stricter lending requirements.

For your start up business, getting approved for an unsecured loan will depend heavily on your personal credit score, business plan and cash flow forecasts. Alternative lenders, including online loan providers, could be a little more flexible than traditional banks in offering unsecured loans to new business ideas.

4 steps to accessing a business loan

If you’re ready to apply for a startup business loan, follow these steps to improve your chances of getting approved fast:

- Nail down your financing needs: Figure out exactly how much capital you need, what the funds will be used for, and what type of loan best lines up with your plans.

- Prepare the paperwork: Gather up all the essential documents, including your business plan, financial statements, tax returns and collateral details if applying for a secured loan. The more organised and detailed your application, the more appealing it will be to lenders.

- Research and compare various lenders: Compare loan products from traditional banks, alternative lenders, and maybe even P2P platforms. Review the interest rates and terms, and weigh up the pros and cons of secured versus unsecured loans and fixed versus variable interest rates.

- Submit your application and negotiate terms: Once you’ve chosen a lender, lodge your application and be prepared to discuss and negotiate terms.

As a time-poor – and likely cash-poor – startup business owner, getting a loan can be a long and stressful process. But with the right knowledge and plenty of preparation, securing funding is absolutely achievable. Now it’s time to discover how a startup loan can be the stepping stone to turning your business idea into reality.